The Dual Nature of Your Payment:

While part of your mortgage payment is the interest, the other slice goes directly toward reducing your loan principal. This means with every payment, your debt decreases, and your ownership of the asset grows – this is ‘building equity’.

Appreciation in Value:

Over time, the real estate market has shown a tendency to appreciate. A $300,000 house could, given a 3% annual appreciation rate, balloon to over $400,000 in ten years.

Monthly Breakdown of Appreciation:

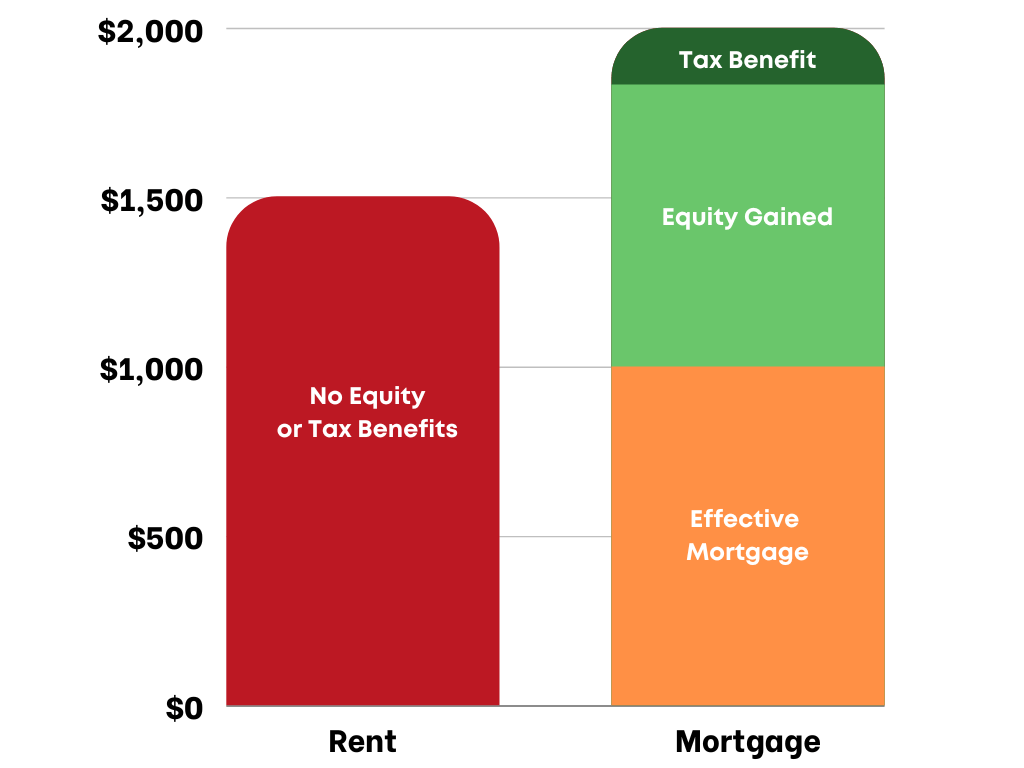

Dividing the $100,000 appreciation over ten years and then monthly, we’re looking at an equity gain of about $830/month. This isn’t money you see now, but it’s wealth being added to your portfolio.

Mortgage Minus Equity Gain:

With a $2,000 mortgage and subtracting the monthly equity gain, you’re effectively paying $1,170. Unlike renting, this amount takes into account the value you’re adding to your own asset.